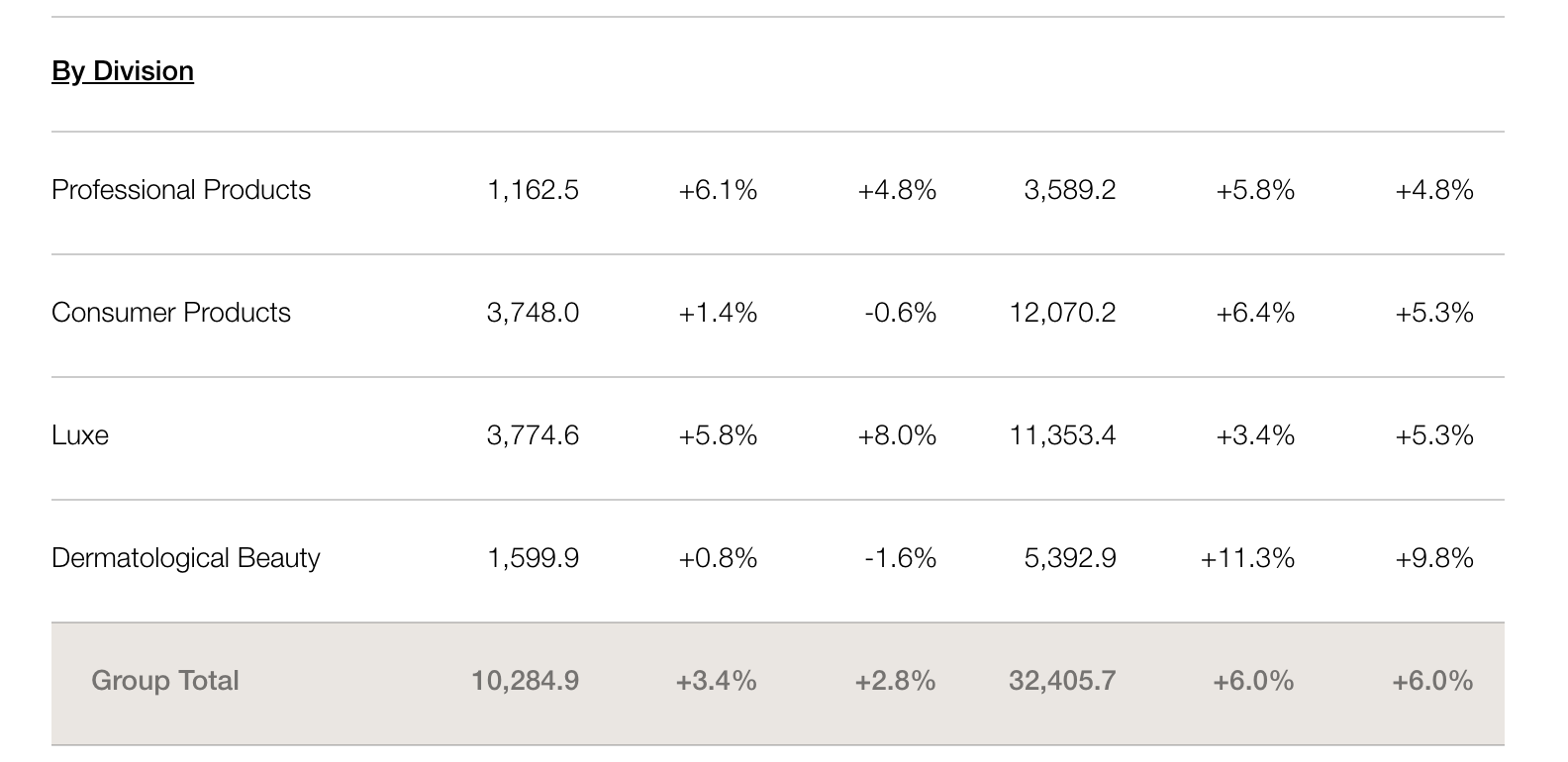

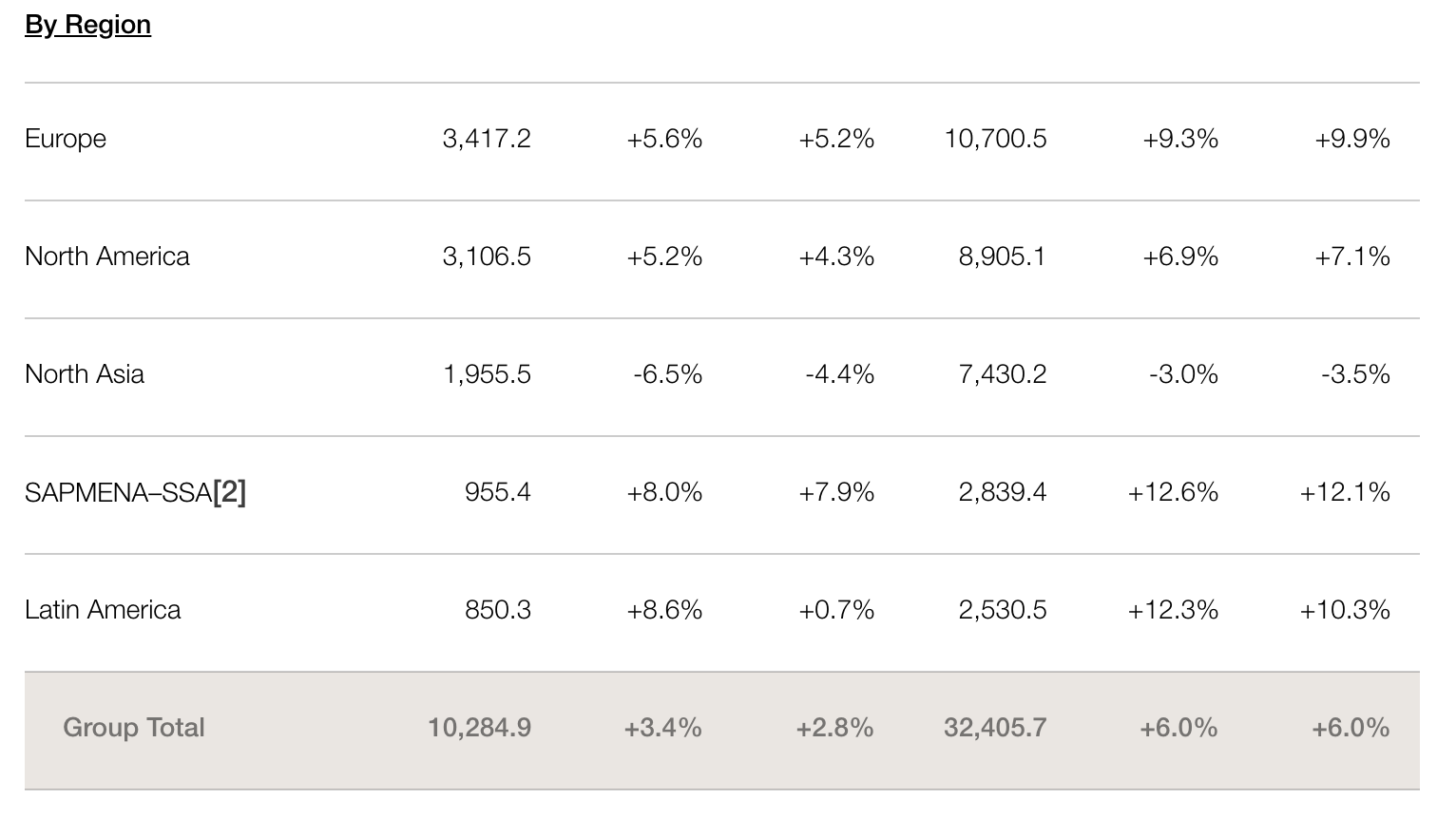

On October 22, French beauty giant L’Oréal Group released its financial results for the nine months ending September 30. Sales increased by 6% year-over-year, reaching €32.4 billion, with constant exchange rate growth of 8.1% and comparable basis growth of 6%. Third-quarter sales rose by 2.8% to €10.28 billion, marking a 3.4% growth on a comparable basis.

Nicolas Hieronimus, CEO of L’Oréal, commented, “We delivered solid growth of +6% in the first nine months, well-balanced between value and volume, despite multiple turbulences that have negatively impacted our third quarter.”

“As anticipated, global beauty market growth has been normalising throughout the year. In the developed markets, this has been driven by a gradual easing in pricing after two years of strong inflation; despite that, underlying market trends remain robust in Europe, and North America – as well as in emerging markets. The situation in the Chinese ecosystem has become even more challenging, but we believe in the future of this market and hope that the governmental stimulus will help improve consumer confidence.”

For the third quarter, sales in the Chinese Mainland declined by single digits, with the Luxury Division experiencing the steepest drop, reaching “negative mid-teens.” Hieronimus noted, “Our performance outpaced a very troubled market, but it is still not good enough.”

By Division

Professional Products Division

This division saw strong growth with a 5.8% increase on a comparable basis and a 4.8% increase on a reported basis over the first nine months.

The division outperformed the global professional market, achieving growth across all regions, including developed markets, North Asia (especially the Chinese Mainland), and emerging markets like the Gulf Cooperation Council, Brazil, and Mexico.

Supported by an omnichannel strategy, the Professional Products division saw robust growth in e-commerce and selective distribution.

The dynamic haircare segment benefited from launches like Kérastase’s Première and Elixir Ultime, while L’Oréal Professional’s Absolute Repair Molecular continued to perform well.

In hair color, Redken’s Shades EQ, iNOA, and L’Oréal Professional’s Dia Color delivered strong results.

The launch of the low-energy AirLight Pro hairdryer in France and the U.S. underscored the division’s commitment to bringing advanced technology to the professional hair industry.

Consumer Products Division

The Consumer Products Division recorded a 6.4% comparable basis growth and a 5.3% increase on a reported basis for the first nine months.

Europe remained a strong growth driver, along with key emerging markets like Brazil, Mexico, and India. Although L’Oréal Parisis the top mass-market brand in China, the division continues to face weak consumer demand there. In North America, ongoing softness in the cosmetics segment impacted growth, though recent innovations are expected to bear fruit by early 2025.

All categories experienced growth driven by strong innovation. Haircare, led by L’Oréal Paris’ Elvive with the successful launch of Glycolic Gloss, was the fastest-growing segment. Makeup saw a boost with Panorama Mascara from L’Oréal Paris, Buttermelt from NYX Professional Makeup, and Teddy Tint from Maybelline New York gaining traction in Southeast Asia. In skincare, Garnier’s Vitamin C Daily Sunscreen found success, while L’Oréal Paris introduced Bright Reveal and Glycolic Bright for spot correction. Garnier also pursued both premiumization and democratization strategies in hair color, supporting its Good series while launching the highly accessible Color Sensation.

Luxury Division

The Luxury Division saw 3.4% growth on a comparable basis, marking its third consecutive quarter of acceleration, with a 5.3% increase on a reported basis.

Double-digit growth continued in North America and emerging markets, while Europe maintained strong momentum. Despite a challenging beauty market in the Chinese Mainland and Asian travel retail markets, the division performed well, further consolidating its leadership. In Japan, the Luxury Division sustained double-digit growth in a vibrant market.

As the leading player in the fragrance market, the division achieved impressive double-digit growth across high-end brands like Yves Saint Laurent Libre, Valentino Born in Roma, and Prada Paradoxe. Ultra-premium lines, including Maison Margiela Replica and Armani Privé, continued to flourish, with Azzaro and Viktor&Rolf also contributing significantly to growth.

In cosmetics, Yves Saint Laurent enjoyed double-digit growth globally, while Prada expanded ambitiously. Valentino continued to gain traction with its latest innovation, Spike Valentino.

Dermatological Beauty Division

For the first nine months, the Dermatological Beauty Division achieved an 11.3% year-over-year increase on a comparable basis and a 9.8% increase on a reported basis.

Adjusted for last year’s €57 million plant insurance compensation received by Vichy in Q3 2023, the division saw 12.6% growth over the period, continuing to outperform a slowing skincare market, especially in the U.S., and despite lower-value growth contributions and unfavorable weather reducing demand for sun care products.

Both developed and emerging markets reported double-digit growth, with significant expansion in South Asia-Pacific, the Middle East, North Africa, and Sub-Saharan Africa (SAPEMENA-SSA). Strong results were also seen in the Chinese Mainland, the U.S., and Europe.

Leading the growth was La Roche-Posay, fueled by the launch of Mela B3, an innovative product leveraging the patented Melasyl™ molecule to address pigmentation issues. CeraVe maintained market leadership across all regions, with nearly half of its sales now coming from outside the U.S. Vichy also saw double-digit growth, boosted by its Dercos haircare line, while SkinCeuticals accelerated with the release of its professional-grade anti-wrinkle serum, P-Tiox.

Regional Performance

Europe

Sales in Europe grew strongly over the first nine months, rising 9.3% on a comparable basis and 9.9% on a reported basis.

L’Oréal outpaced the market across most countries, particularly in Spain, Portugal, the UK, Ireland, and the Germany-Austria-Switzerland cluster, as well as in various mid-sized countries. All categories experienced double-digit growth, led by haircare and fragrances.

The Consumer Products Division’s growth was driven by the ongoing success of L’Oréal Paris, especially in haircare, along with Garnier in skincare and NYX Professional Makeup.

Luxury Division sustained strong momentum, with fragrances and cosmetics driving growth, while the men’s segment continued to grow robustly.

The Dermatological Beauty Division outperformed the market significantly, led by CeraVe and boosted by La Roche-Posay’s Mela B3.

The Professional Products Division surpassed market growth, supported by Kérastase’s strong performance and successful launches from Redken and Matrix, including the Air Light Pro hairdryer in French salons.

North America

Sales rose by 6.9% on a comparable basis and 7.1% on a reported basis for the first nine months, driven by ongoing channel expansion and value growth.

The Luxury Division led the market, especially in the vibrant fragrance segment, supported by Prada, Valentino, and Yves Saint Laurent’s MYSLF and the launch of Libre Flower & Flames. In skincare, Kiehl’s and Youth to the People benefited from new products and expanded online channels.

In the Consumer Products Division, growth was mainly driven by haircare, with L’Oréal Paris consolidating its position. The division’s performance was disproportionately affected by continued softness in makeup, though new innovations are expected to make an impact.

Dermatological Beauty continued to outperform the market, with La Roche-Posay’s Anthelios and Toleriane performing strongly and SkinCeuticals’ P-Tiox seeing a successful launch.

The Professional Products Division led the market, thanks to strong launches like Kérastase’s Première and Redken’s Acidic Color Gloss, along with an effective omnichannel strategy.

North Asia (including the Chinese Mainland, Hong Kong, Taiwan, South Korea, and Japan)

Sales declined by 3.0% on a comparable basis and 3.5% on a reported basis over the first nine months.

In the Chinese Mainland, consumer confidence weighed on the beauty market, which had already shown negative growth in the second quarter. Sales saw a slight single-digit decline as the Luxury Division continued to gain market share, though challenges remain. The Dermatological Beauty and Professional Products Divisions also grew above their market averages.

Although travel retail saw a return to growth in Q3, Hainan remains under pressure. In Japan, L’Oréal’s performance surpassed the market average, supported by both domestic consumers and tourists, making it the leading international beauty company.

In North Asia, the Dermatological Beauty Division grew at double digits, outpacing the market with strong contributions from its three main brands. The Professional Products Division, buoyed by Kérastase, exceeded market performance, while the Luxury Division held its ground, led by high-end products like Lancôme’s Génifique and Prada Rouge. Aesop maintained an active presence in the Chinese market. L’Oréal Paris saw single-digit growth in the Consumer Products Division.

South Asia-Pacific, Middle East, North Africa, and Sub-Saharan Africa (SAPEMENA-SSA)

For the first nine months, sales in the SAPEMENA-SSA region grew by 12.6% on a comparable basis and 12.1% on a reported basis.

Growth in the South Asia-Pacific, Middle East, and North Africa regions (SAPMENA) was broadly based, with all divisions and categories contributing through a balanced mix of value, product assortment, pricing, and volume.

Key growth drivers by country included the Australia-New Zealand cluster, Thailand, Saudi Arabia, India, and Vietnam.

By division, the strongest performance came from Dermatological Beauty, with CeraVe’s continued success. The Luxury Division also saw double-digit growth, driven by Yves Saint Laurent and Prada.

Online sales remained particularly robust, especially in Saudi Arabia, India, and Southeast Asia.

Fragrance was the fastest-growing category, spurred by new product launches, while skincare benefited from strong performances in dermatological and consumer products. Both mass and professional haircare segments saw continued premiumization, driving haircare growth.

The Sub-Saharan Africa (SSA) region posted exceptional growth, with double-digit gains across all countries and divisions. By category, facial care achieved record-breaking growth, followed by haircare. The Consumer Products and Dermatological Beauty divisions were primary growth drivers.

Latin America

In Latin America, sales for the first nine months increased by 12.3% on a comparable basis and 10.3% on a reported basis, supported by balanced contributions from both value and volume.

Performance was broad-based across the region, with standout results in Mexico and Brazil. Argentina, however, faced challenges due to economic instability and reduced consumer spending.

By division, the Consumer Products Division maintained strong momentum, with L’Oréal Paris especially active. Elsève reinforced its value leadership in Brazil’s haircare market. Luxury growth was propelled by strong results in Mexico.

Haircare remained a standout category across all divisions, with makeup and fragrance also seeing robust growth.

Online channels continued to drive growth across the region, supported by the strong performance of pure e-commerce players.

“Overall, the beauty sector continues to grow in both product sales and resilience, demonstrating its long-term potential,” summarized CEO Nicolas Hieronimus. “L’Oréal’s strong performance reflects our innovation, team agility, and ability to reallocate resources to new growth engines.” He added, “Amid ongoing economic and geopolitical uncertainties, we remain confident in achieving both sales and profit growth this year and are actively preparing our 2025 beauty acceleration plan.”

Since June, L’Oréal’s stock has declined by over 20%, erasing about €50 billion in market value due to investor concerns about the consumer outlook in China. As of 12:30 p.m. on October 23, the stock traded at €353.6, down 3.7% from the previous day, with a market capitalization of approximately €193.5 billion.

Key Developments Since L’Oréal’s Mid-Year Report in July

Strategy:

- In August, L’Oréal announced the acquisition of a 10% stake in Swiss skincare group Galderma GALD.S, the parent company of Cetaphil, though the transaction amount was undisclosed. The partnership aims to combine Galderma’s dermatological expertise with L’Oréal’s knowledge in skin biology, diagnostics, and assessment methods.

Research, Beauty Tech, and Digital:

- In September, L’Oréal entered a partnership with biotech innovator Abolis Biotechnologies and specialty chemicals manufacturer Evonik to co-develop sustainable ingredients for beauty and other products.

- At October’s Dermatology Alliance Forum, L’Oréal’s Dermatological Beauty Division and the International League of Dermatological Societies (ILDS) announced a landmark study to assess the availability and accessibility of dermatology services across 194 countries.

Environmental, Social, and Governance (ESG) Performance:

- In September, Fast Company named L’Oréal among the top 50 most innovative workplaces for 2024, recognizing it in the Beauty & Fashion category.

- L’Oréal also ranked fifth globally and first in France on FTSE Russell’s 2024 Diversity & Inclusion Index.

- In addition, L’Oréal achieved high scores on the 2024 Disability Equality Index by Disability, acknowledging its commitment to diversity, equity, and inclusion.

Other:

- In celebration of Fashion Week, L’Oréal’s seventh “Walk Your Worth” event was held at the Paris Opera House, with live viewership exceeding 1.1 million.

|Source: Official Financial Report, Reuters, Luxeplace Historical Articles

|Image Credit: Official Website

|Editor: LeZhi