As the global luxury goods industry enters a historic trough, the significance of Chinese consumers and the domestic market continues to grow. One of the most telling signs: since the latter half of last year, numerous senior executives from major international luxury brands have been flocking to China’s key cities to conduct in-depth store visits. At their annual financial results briefings, they have been candidly sharing their observations with financial analysts.

It is evident that in China’s maturing luxury market, major brands now confront a series of novel challenges. From brand communication and product planning to store deployment and operations, securing tomorrow’s success demands significantly enhanced management precision and local market insight.

As the most crucial ‘dashboard’ for China’s luxury market, LUXE.CO launched the ‘Luxury Brands in China Power Ranking’ (link) has consistently presented a systematic overview of major brands’ expansion efforts, investment levels, and strategic positioning in China market. Grounded in robust proprietary data and analytical frameworks, it offers unique insights into the market’s activities and emerging trends. This provides invaluable reference for brand and commercial property managers seeking to gauge the pulse of China market, understand competitive landscapes, and learn industry best practices.

On the eve of the Year of the Horse Spring Festival, LUXE.CO hosted an online briefing for the 2025 Luxury Brands in China Power Ranking, attracting enthusiastic participation from professionals across luxury brands, apparel companies, commercial real estate firms, securities houses, private equity funds, major internet corporations, and international PR agencies.

Drawing upon the 2025 ranking scoring and the latest research from the LUXE.CO INTELLIGENCE, LUXE.CO Founder/CEO Alicia Yu and LUXE.CO Senior Vice President Elisa Wang shared ten key insights into China’s luxury market during the session:

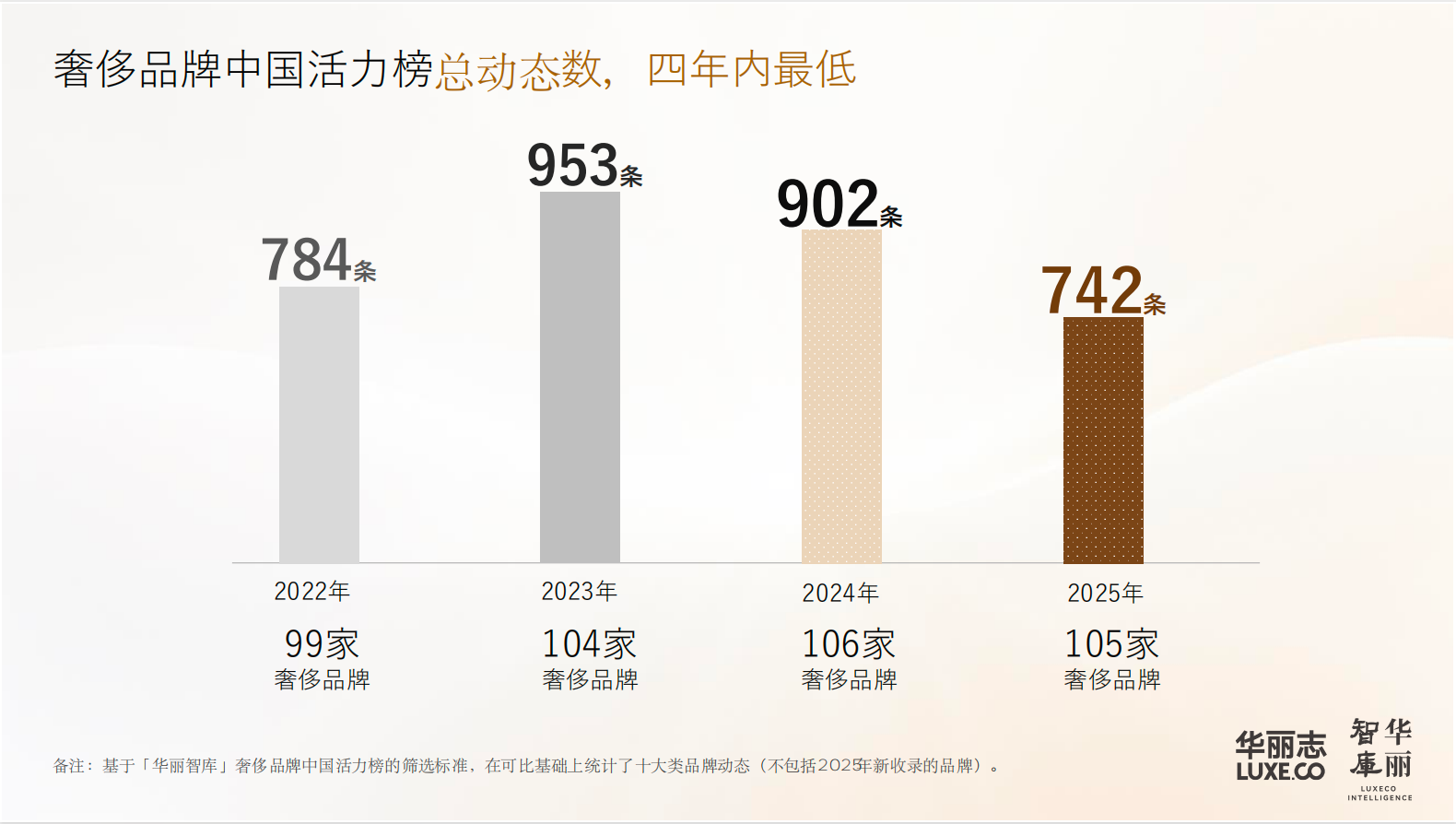

- Overall activity among international luxury brands reached its lowest level in four years.

- Leading brands demonstrated the highest investment intensity and stability in China market.

- Fine jewellery brands exhibited the strongest resilience, with their share in the Top 10 of the ranking increasing annually.

- Domestic luxury brands achieved breakthroughs, with Lao Pu Gold rising to the Top 3 in the ranking.

- Luxury brand store expansion slowed by approximately 30%, with non-tier-one cities experiencing greater impact.

- Store expansion and upgrades remain paramount.

- The “quiet luxury” trend is gaining momentum, with three representative brands expanding accordingly.

- Chinese cultural elements and Eastern aesthetics are key factors in appealing to domestic fine consumers.

- Hong Kong and Beijing have emerged as new hotspots for luxury brands to establish stores and host events.

- Four core “hard strengths” provide a solid foundation for luxury brands navigating headwinds.

Insight 1:

Overall activity among international luxury brands hits four-year low.

The Luxury Brands in China Power Ranking recorded 742 activities involving 105 luxury brands in China market – the lowest tally in four years, even falling below 2022 levels during the pandemic’s final stages.

Even Bernard Arnault, Chairman and CEO of the LVMH Group who has weathered multiple economic cycles, laments that the luxury sector is enduring a bitter ‘winter’.

Insight 2:

Leading Brands Maintain Highest Investment and Stability in China Market.

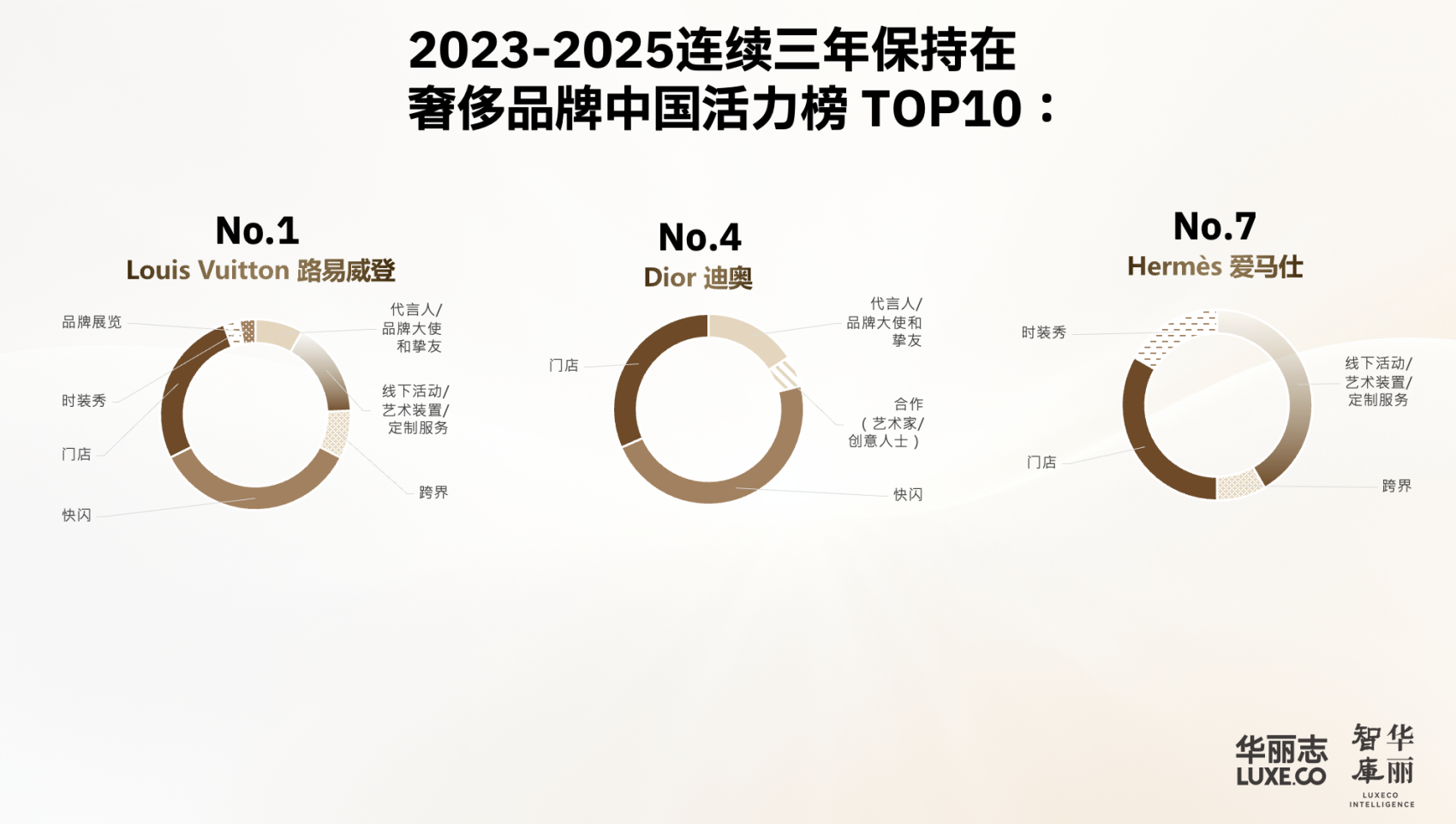

Despite the deep freeze, the most prestigious ‘leading’ brands in the luxury sector have sustained their investment and activity levels in China market: Louis Vuitton, Dior, and Hermès have all featured in the Top 10 for three consecutive years.

Among them, Louis Vuitton—the world’s highest-grossing luxury brand—has claimed the top spot on the ranking for three consecutive years.

Jean-Jacques Guiony, former Chief Financial Officer of the LVMH Group, once remarked: ‘There have always been questions about Louis Vuitton’s capacity for further growth… yet it consistently achieves new breakthroughs.’

Analysing brand dynamics from the the Luxury Brands in China Power Ranking perspective (see below), Louis Vuitton’s investments in China demonstrate remarkable diversity, surpassing most listed brands in richness. This indicates that the sustained growth of the Louis Vuitton brand is underpinned not by a single winning formula, but by a persistently efficient and complex system. It is within this framework that truly groundbreaking innovations (such as the ‘Louis’ ship in Shanghai) are conceived.

Dior underwent an intensive round of creative and management restructuring in 2025, with J.W Anderson becoming the first ‘omnipotent’ creative director since founder Christian Dior to oversee all brand collections. During this generational transition, the brand’s activity inevitably dipped. According to the ranking, Dior’s dynamic metrics in China market were only about half those of Louis Vuitton.

In contrast, Hermès prioritises steadfast consistency. As Executive Chairman and CEO Axel Dumas stated: “Over recent years, we have not cancelled a single project [in China]. We continue advancing our plans according to established strategies. … We currently operate 32 stores in China, maintaining considerable stability. Growth will proceed at our own pace, gradually. What is certain is our long-term perspective. We do not adopt a stop-start approach.”

Insight 3:

Fine jewellery brands demonstrate strongest resilience, with their share of the Top 10 increasing annually.

Precious materials, timeless designs, exquisite craftsmanship, and a degree of investment appeal collectively make fine jewellery a more accessible luxury purchase in the current economic climate, establishing it as the most resilient category. In contrast to the relative quiet of apparel and leather goods brands, jewellery brands have seen a sharp rise in investment and activity within China’s luxury market.

Over the past three years, changes in the Luxury Brands in China Power Ranking vividly illustrate this trend. The number of fine jewellery brands in the Top 10 has grown from one in 2023 to three in 2024, and is projected to reach four in 2025 (Tiffany & Co., Lao Pu Gold, Van Cleef & Arpels, Qeelin).

Insight 4:

Domestic Luxury Brands Break Through, with Laopu Gold Surging to the Top 3.

2025 stands as a breakthrough year for China’s domestic luxury brands, with two jewellery houses (Laopu Gold and Chow Tai Fook) making their debut on the Luxury Brands in China Power Ranking.

Chow Tai Fook formally entered the ‘Haute Joaillerie’ segment, distinguishing itself with Eastern aesthetics in a field long dominated by international heavyweights. Old Gold (LAOPU GOLD) achieved a milestone by establishing a presence in China’s top ten ‘premium luxury’ shopping centres. Its outstanding performance has exerted significant pressure on international peers and prompted multiple global financial institutions to take notice of the strength of China’s domestic luxury brands.

As the luxury brand with the most aggressive store expansion in China’s market in 2025, Laopu Gold secured third place in its debut on the ranking, propelled by an exceptionally high score in the ‘Store Expansion’ category. Moving forward, we anticipate Laopu Gold and other Chinese brands making a stronger impact across additional marketing dimensions.

Insight 5:

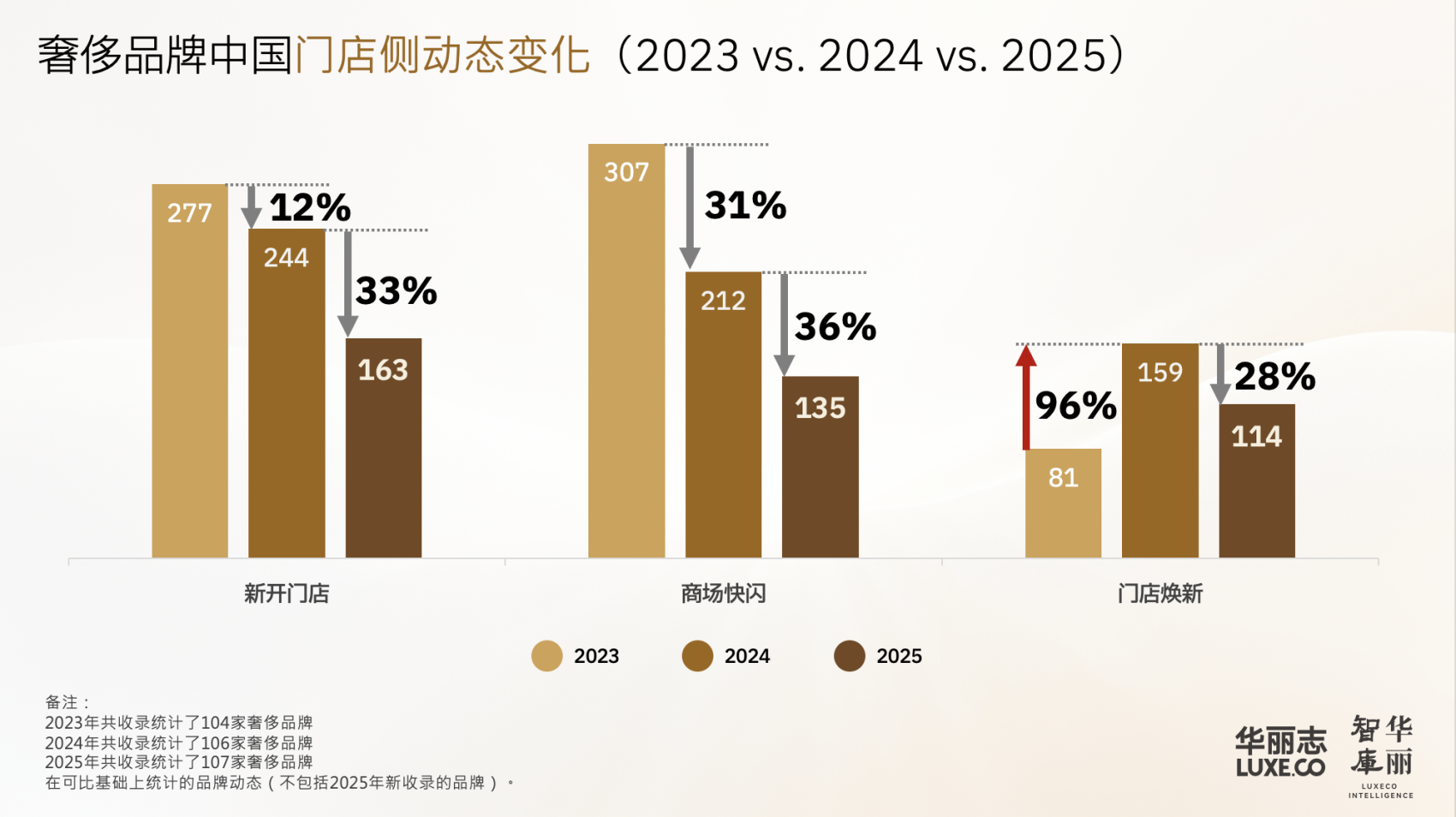

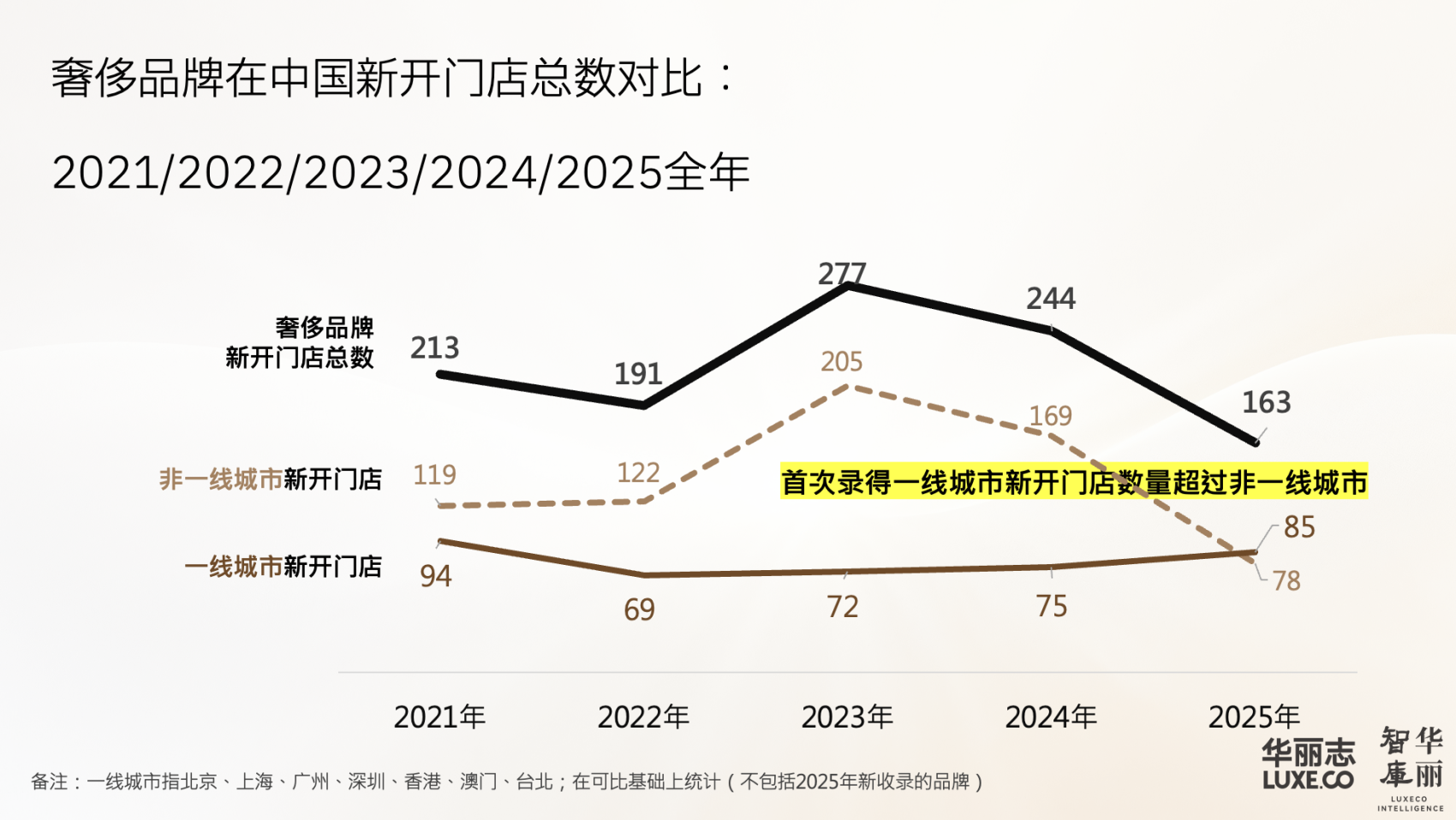

Luxury brand store expansion declines by approximately 30%, with non-tier-one cities bearing greater impact.

Data from the ranking reveals that in 2025, the total number of new luxury brand stores opened decreased by 33% compared to 2024. The volume of mall pop-ups fell by 36%, while refurbished stores declined by 28% from the relatively high base of 2024.

Evidently, after nearly two decades of rapid expansion, luxury brands—particularly established players with substantial existing store networks—are now optimising their retail footprints. This involves re-evaluating city and mall locations, even adjusting in-mall positioning, to reduce unnecessary expenditure and navigate the current downturn.

As articulated by the head of Zegna Group: ‘ZEGNA’s substantial store footprint in China has become a burden under current conditions, which is why the brand is now committed to “streamlining”.’ By closing underperforming outlets, the brand will undertake a ‘rationalisation’ of its Chinese store network to concentrate resources on delivering superior customer experiences.

Such adjustments are expected to continue through 2026, with fine shopping centres and commercial districts facing sustained pressure. Industry attention will focus on which brands will fill the vacancies left by luxury retailers’ closures.

Notably, for the first time in the past four years, the report recorded more new luxury store openings in first-tier cities than in non-first-tier cities.

This signals luxury brands’ heightened focus on return on investment for store expansion, concentrating efforts on top-tier cities and commercial districts with higher potential sales per square metre. For instance, despite Zegna’s impending closure of 10 stores in China, it plans to open a new outlet in Shenzhen Bay, citing ‘(Shenzhen) being a crucial city’.

Insight 6:

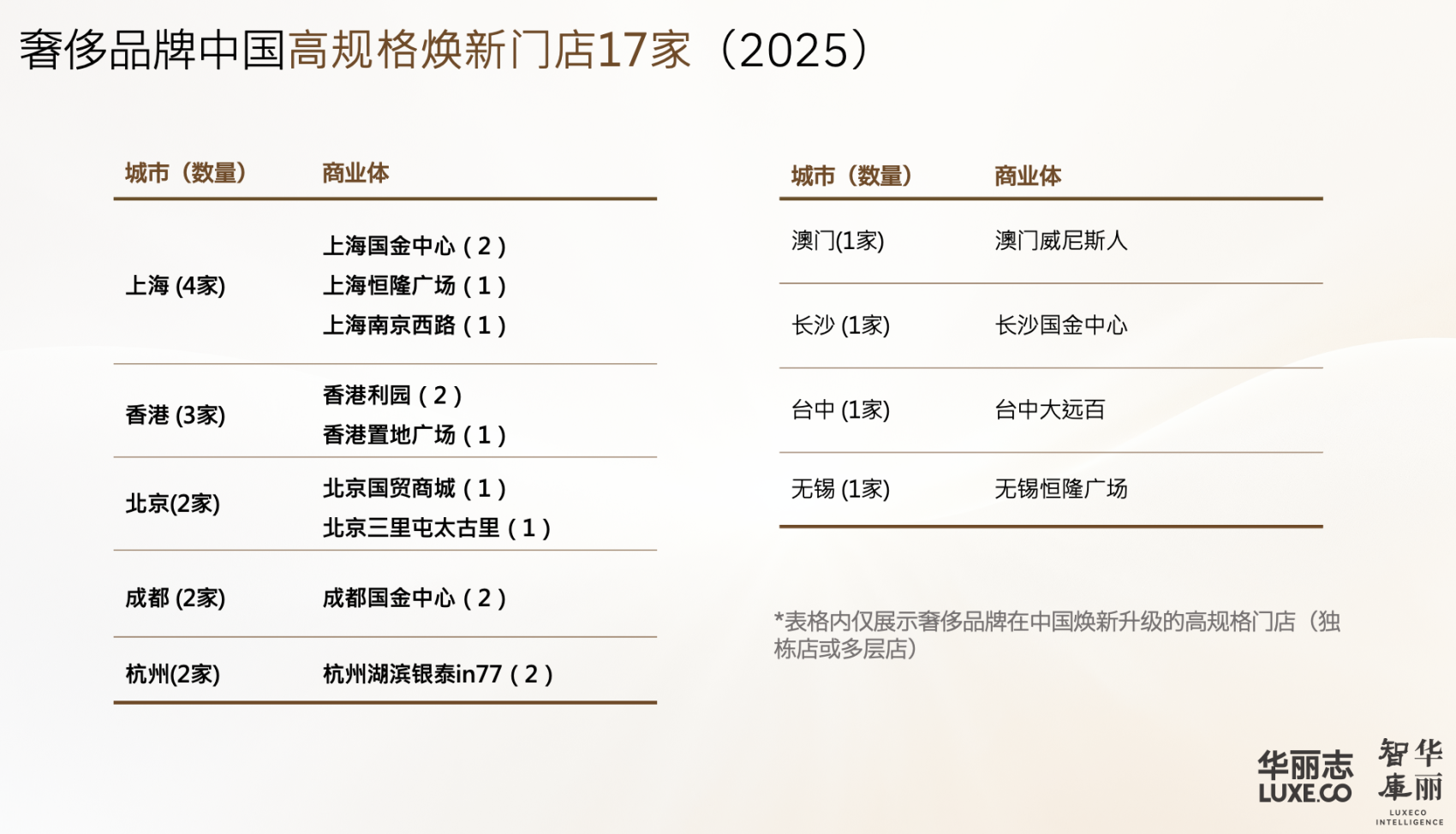

Store Expansion and Upgrades Remain Paramount.

Data from the report reveals that by 2025, ‘stores’ will remain a key focus for multiple leading luxury brands. Through store dynamics, we can observe which brands are accelerating market share capture during market downturns.

Take Tiffany & Co., which surged to the Top 2 in the 2025 Vitality Ranking: last year, the brand completed the opening and refurbishment of eight stores across China market. In fact, since the LVMH Group’s full acquisition of Tiffany in early 2021, store upgrades and renovations have been a top priority.

Regarding the significance of this initiative, Stéphane Bianchi, CEO of the LVMH’s Watches and Jewellery division, noted: ‘By the end of 2025, Tiffany’s new-concept stores will account for approximately one-third of the total store count, contributing 42% of sales – up from 31% previously. The performance gap between new and legacy stores stands at around 15 to 20 percentage points. This bodes extremely well for the future.’

Additionally, Canada Goose’s significant rise in the ranking for 2025 (up 27 places from 2024) was underpinned by the opening of seven new stores, with its direct-to-consumer (DTC) channel in mainland China outperforming all other core global markets.

Insight 7:

The “quiet luxury” trend gains momentum as three representative brands expand

Over recent years, “quiet luxury” or so-called “old money” aesthetics have gained considerable favour among China’s fine consumers. Quiet luxury brands have consequently increased their investment, with three representative names seeing their rankings soar on the ranking.

Among them, Loro Piana entered the annual Top 10 for the first time in 2025.

In March 2025, to mark its centenary, Loro Piana launched its inaugural global exhibition ‘A Century’s Touch’ in Shanghai. This landmark event spanned three galleries and 15 exhibition rooms, covering over 1,000 square metres. That year, the brand opened or refurbished seven new stores in China, including two multi-level boutiques.

Compared to 2024, Brunello Cucinelli (11th place) climbed 22 positions on the ranking. In 2025, the brand significantly intensified its channel expansion in China, opening or refurbishing nine stores – a figure substantially higher than previous years.

Ralph Lauren (12th place) also climbed 17 positions. In 2025, the brand held its first Asian show in Shanghai and staged ten events across Hong Kong, Beijing, Shenyang, Wuhan, Hangzhou, Nanjing, and Guangzhou.

Insight 8:

Chinese cultural elements and Eastern aesthetics emerge as pivotal factors in resonating with domestic luxury consumers

The resurgence of traditional culture is unstoppable, with Chinese cultural motifs and Eastern aesthetics becoming crucial assets for luxury brands to captivate Chinese consumers.

Old Shop Gold, which entered the rankings directly into the Top 3, revived ‘traditional Chinese gold techniques’. From brand philosophy and product development to in-store experiences, elements and concepts of ‘classical culture’ are woven throughout.

Since 2017, Chow Tai Fook has successively launched jewellery collections rich in traditional cultural significance and Eastern aesthetics, including the Heritage, Fortune, Joy, and Forbidden City series. Both the Fortune and Forbidden City collections achieved sales of approximately HK$4 billion in the 2025 financial year.

Qeelin, founded in Hong Kong and now part of France’s Kering Group, has seen its ranking on the ranking rise annually, entering the Top 10 for the first time in 2025. Its iconic Gourd Collection has gained widespread recognition, and in 2025 collaborated with multiple artists to reinterpret traditional art forms such as intangible cultural heritage paper crafts and cloisonné enamel.

Christophe Artaux, the brand’s CEO, once told Luxe.co: “Cultural relevance is paramount. Customers perceive a strong connection with our fine jewellery pieces. Our designs narrate familiar stories or symbols, allowing people to reconnect with cultural moments in a deeply emotional way.”

Insight 9:

Hong Kong and Beijing emerge as new hotspots for luxury brand store openings and events

As previously noted, luxury brands are refocusing their store investments towards first-tier cities.

Among the top five cities for new store openings in 2025, Hong Kong’s resurgence is particularly noteworthy.

Regarding marketing activities, we observe Beijing’s growing prominence year on year, as more luxury brands recognise the immense consumer potential within this political and cultural hub. Simultaneously, the vast northern market served by Beijing warrants significant investment and cultivation.

Insight 10

Four Core Competencies Form the Steadfast Foundation for Luxury Brands Navigating Headwinds

Each time the rankings are unveiled, we gain a clear perspective on the transformations occurring within China’s luxury market over the preceding year. In 2025, these shifts have been particularly pronounced.

As the luxury sector enters a cyclical downturn, particularly with China’s market no longer expanding as expansively as before, the gap between brands may quietly widen. Through the data and facts behind the ranking, we observe that the following four long-cultivated ‘hard strengths’ form the robust foundation enabling luxury brands to navigate headwinds:

The brand’s own recognition and reputation

The operational and financial strength of the brand and its parent group

The perceived value and investment appeal of the brand’s core products

A deeper understanding of China market and more proactive strategies among global management

——Conclusion——

Looking ahead, Bernard Arnault, Chairman and CEO of the LVMH Group, recently stated, “One thing I am certain of is that the desire for high-quality products goes hand in hand with the rise in living standards across the world, and this trend is here to stay. While there will be ups and downs in certain countries, the global trend is clear. So in the long run, we can be optimistic.”

Bain & Company, in collaboration with Altagamma (the Italian Luxury Brands Association), recently released its 2025 China Personal Luxury Goods Market Report, which projects that China’s luxury market will sustain its recovery momentum in 2026.

Luxe.CO and our readers are witnessing China’s luxury market navigate their first full business cycle in China: explosive growth > slowdown > stabilization > recovery. Meanwhile, the evolving preferences of Chinese consumers and the rise of homegrown Chinese brands are placing ever-higher demands on the localized management capabilities of international luxury houses.

As Alicia Yu, Founder of Luxe.CO, noted: “Exemplified by the Luxury Brands in China Power Ranking, data-driven brand and industry research is growing in importance by the day. Only by continuously eliminating cognitive blind spots, and proactively reflecting on and exploring new approaches, can luxury industry practitioners keep pace with the times and strive for excellence. We hope that the industry will focus on building internal capabilities during this trough, and adjust strategies in a more prudent and proactive manner to seize the first-mover advantage when the next growth cycle of China’s high-end consumption market arrives.”

丨Editor: Elisa Wang