On May 12, Swiss sportswear company On Holding AG reported its results for the first quarter of fiscal year 2026 ending March 31. Driven by the advantages of its premiumisation strategy, disciplined operational execution, and demand across all markets, both net sales and profitability reached record highs. Net sales increased by 14.5% year-on-year to CHF 831.9 million (at constant exchange rates: +26.4%). Revenue in the Asia-Pacific market rose by 44.4% year-on-year to CHF 450.7 million (at constant exchange rates: +61.4%), contributing more than 20% of global net sales, with particularly strong performances in China and South Korea.

This also marks the first time that On’s quarterly net sales have exceeded the CHF 800 million milestone. Gross profit rose by 22.8% year-on-year to CHF 534.3 million; adjusted EBITDA increased by 45.4% to CHF 174.3 million; and net profit surged by 82.2% to CHF 103.3 million.

On noted that both its direct-to-consumer (DTC) and wholesale channels delivered strong growth, demonstrating the brand’s ability not only to deepen engagement with existing customers but also to continuously attract new consumers globally.

At the same time, On has completed a top-level management reshuffle: co-founders David Allemann and Caspar Coppetti officially assumed the role of Co-CEOs on May 1. Frank Sluis, formerly of retail group Ahold Delhaize, joined as Chief Financial Officer.

Caspar Coppetti said that “Q1 was an outstanding start to the year and another strong proof point of our premium strategy in action. On is becoming more global, more multi-dimensional and more deeply rooted in different communities around the world. As David and I step into our new roles as Co-CEOs, we do so with strong commitment to the continuity of our strategy, values and entrepreneurial spirit that have defined On over the past 16 years. I also want to express our heartfelt gratitude to our dear friend and partner Martin. His leadership helped build the financial strength, operational rigor and clarity that have brought us to this moment. As we continue to scale from this very strong foundation, we believe the next chapter of On can be even stronger as we continue to Dream On.”

Outgoing CEO and CFO Martin Hoffmann said that “These results show the quality of On’s growth and the strength of the financial foundation we have built. Since our IPO nearly five years ago, we have more than quadrupled our net sales, strengthened our premium positioning and built a financial profile that reflects the incredible ambition of the brand. The results we present today – highlighted by record net sales and a gross profit margin of 64.2% – demonstrates our unique ability to scale rapidly while expanding our profitability. I am incredibly proud to hand over at a time when On is stronger than ever, with clear momentum, an extraordinary team and an exciting future ahead. My deepest thanks go to our Founders, the whole On team, and to the investor and analyst community for their trust and partnership over the years.”

New CFO Frank Sluis stated that “In my first weeks with On, I have been struck by the strength of the culture, the clarity of vision and purpose, and the high ambition across the company. I look forward to building on the momentum – supporting long-term growth, preserving the premium economics of the brand, and helping On continue to scale with agility, discipline and entrepreneurial energy.”

Benefiting from strong product demand, disciplined full-price sales management, and efficient operations, On delivered record profitability in the first quarter. Despite significant headwinds from increased U.S. tariffs, gross margin rose by 430 basis points year-on-year to 64.2%, while adjusted EBITDA margin reached 21%. The company translated improvements in gross margin and operational efficiency into profit growth while continuing to invest in long-term high-growth opportunities. Net profit margin reached 12.4%.

Supported by a strong pipeline of product innovation and iconic brand marketing campaigns, On further strengthened its positioning at the intersection of athletic performance, design aesthetics, and cultural relevance. LightSpray technology has moved from validation among professional athletes to broader commercialisation, with the successful launch of the flagship LightSpray Cloudmonster 3 Hyper. Meanwhile, lifestyle products such as the Cloudtilt Remix have performed strongly, highlighting the brand’s growing influence among fashion-forward sneaker consumers.

Caspar Coppetti said that “LightSpray Cloudmonster Hyper sold out rapidly across multiple channels, with particularly strong demand in Asia-Pacific and the U.S. During the first week of our new Boston store opening, LightSpray products accounted for nearly 20% of footwear net sales. Currently, daily sales through DTC channels alone reach several hundred pairs. For a technology still in the early stages of commercialisation, this level of demand is highly encouraging.”

Speaking further at the analyst call, Caspar Coppetti noted that “consumers today are increasingly willing to pay for differentiated products, which is precisely our core competitive advantage. By continuously innovating at the intersection of performance, design, and sustainability, we deliver a unique, high-quality brand experience. Through omnichannel engagement and touchpoints, we are building long-term brand equity to support sustained growth. This is central to our ambition of becoming a leading global premium sportswear brand.”

Caspar Coppetti added that a new generation of consumers without age boundaries increasingly views health as a form of wealth and sportswear as a marker of identity rather than purely functional apparel. “They are drawn to premium brands with cultural influence that combine athletic performance with lifestyle appeal. This has driven strong growth in our lifestyle category this quarter.”

He further noted that collaborations with leading brands in the sneaker and streetwear space have enabled On to attract younger consumers while maintaining a high-quality profit model and reinforcing its premium positioning. Highly sought-after collaborations, including the reissued Cloudswift and a full women’s collection developed with Zendaya, demonstrate how the brand continues to build credibility in new communities through design, culture, and premium products.

In the first quarter, the proportion of consumers aged 18–24 within DTC channels increased significantly, marking the largest rise on record, with the trend accelerating further at the beginning of the second quarter. Brand research conducted during the quarter also showed notable improvements in both perceived athletic performance and the distinctiveness of design.

Caspar Coppetti told Reuters that “from a long-term growth perspective, our expansion into the apparel category and the lifestyle running segment is already showing very encouraging early signs of growth.”

Raymond James analyst Rick Patel commented that On has performed “extremely well” in managing inflation-related costs, and could further benefit from potential U.S. tariff refunds in the future.

Analysts at Jefferies noted that On’s management is focusing heavily on growth in Asia, while cautioning that a slowdown in the U.S. market could weaken its margin leadership over the long term. Influenced by this view, despite rising in pre-market trading, the company’s share price fell by around 4% during early trading.

As of the close on May 12, On’s share price declined by 0.63% from the previous trading day to USD 33.83, with a latest market capitalisation of USD 11.278 billion. Over the past 12 months, the stock has fallen by a cumulative 34.07%.

In October this year, On will host its inaugural On Global Run Summit in Paris, inviting 100 of its core running channel partners worldwide to attend.

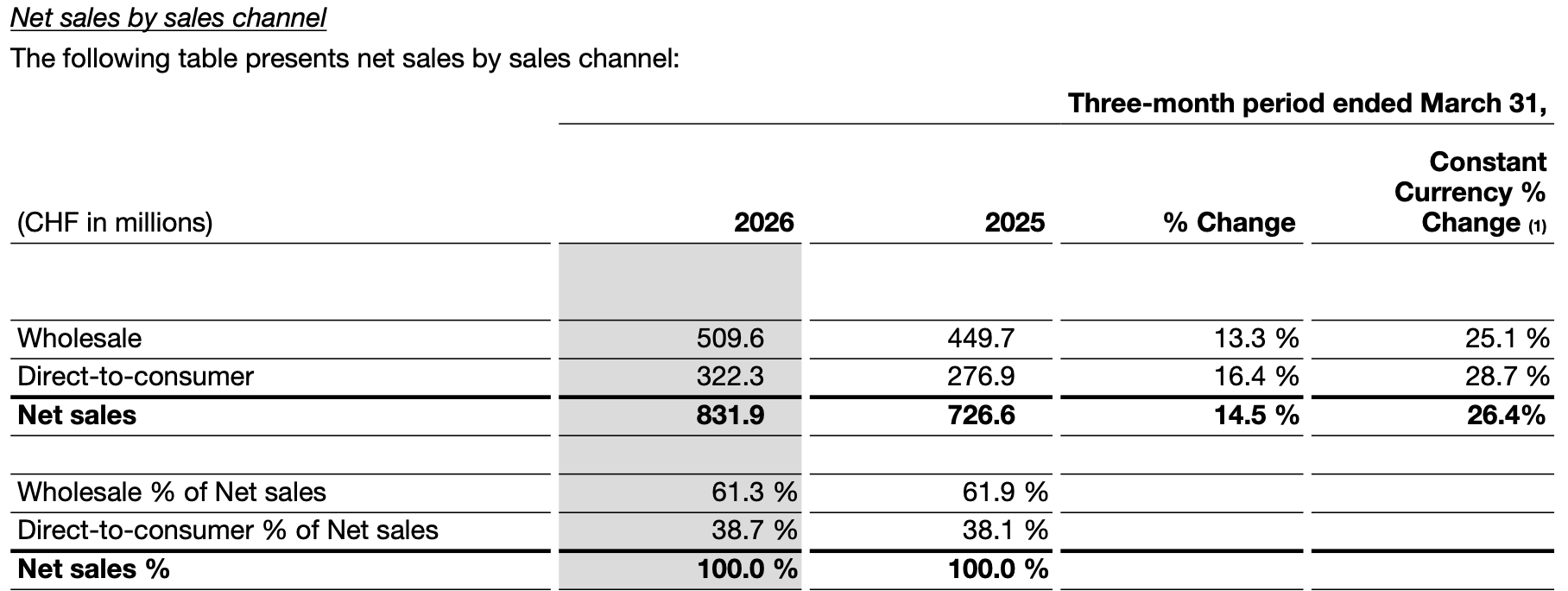

By channel:

- Wholesale channel: net sales increased by 13.3% year-on-year to CHF 509.6 million, up 25.1% at constant exchange rates

- DTC channel: net sales increased by 16.4% year-on-year to CHF 322.3 million, up 28.7% at constant exchange rates

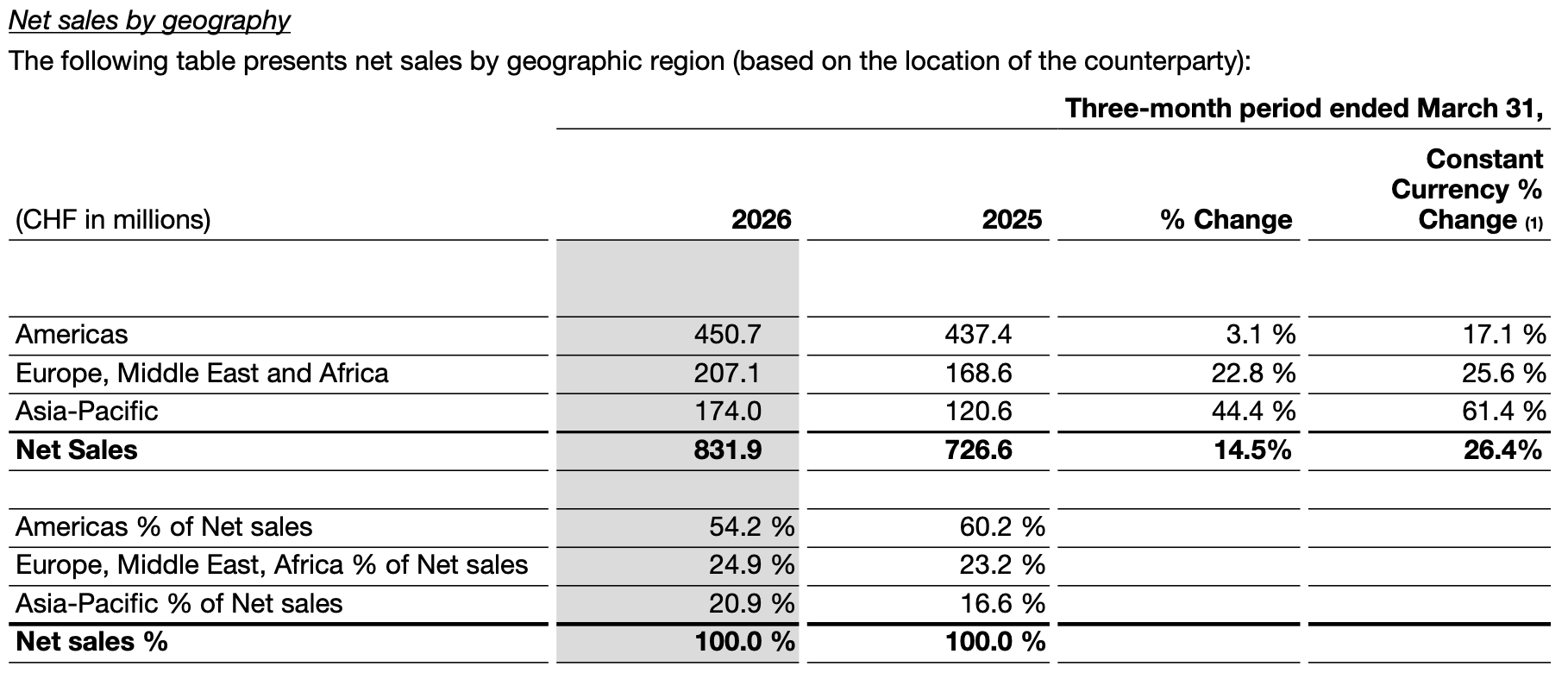

By geographic market:

- Europe, Middle East and Africa (EMEA): net sales rose by 22.8% year-on-year to CHF 207.1 million, up 25.6% at constant exchange rates. Growth was broad-based across multiple countries with solid fundamentals. The UK saw particularly strong momentum driven by its vibrant sneaker culture and large running community, while Germany maintained steady, healthy growth. Despite complex geopolitical conditions in the Middle East, the region delivered strong results, further demonstrating the company’s broad-based growth and resilience.

- Americas: net sales increased by 3.1% year-on-year to CHF 450.7 million, up 17.1% at constant exchange rates, mainly impacted by foreign exchange headwinds. Brand awareness in the region continues to rise, with premium operations and full-price sales strategies firmly executed. Overall brand awareness surpassed 30% for the first time, marking a significant milestone.

- Asia-Pacific: net sales surged by 44.4% year-on-year to CHF 174.0 million, up 61.4% at constant exchange rates. Growth was balanced across sub-regions and channels, with Greater China significantly outperforming the regional average. Net sales in South Korea more than doubled year-on-year.

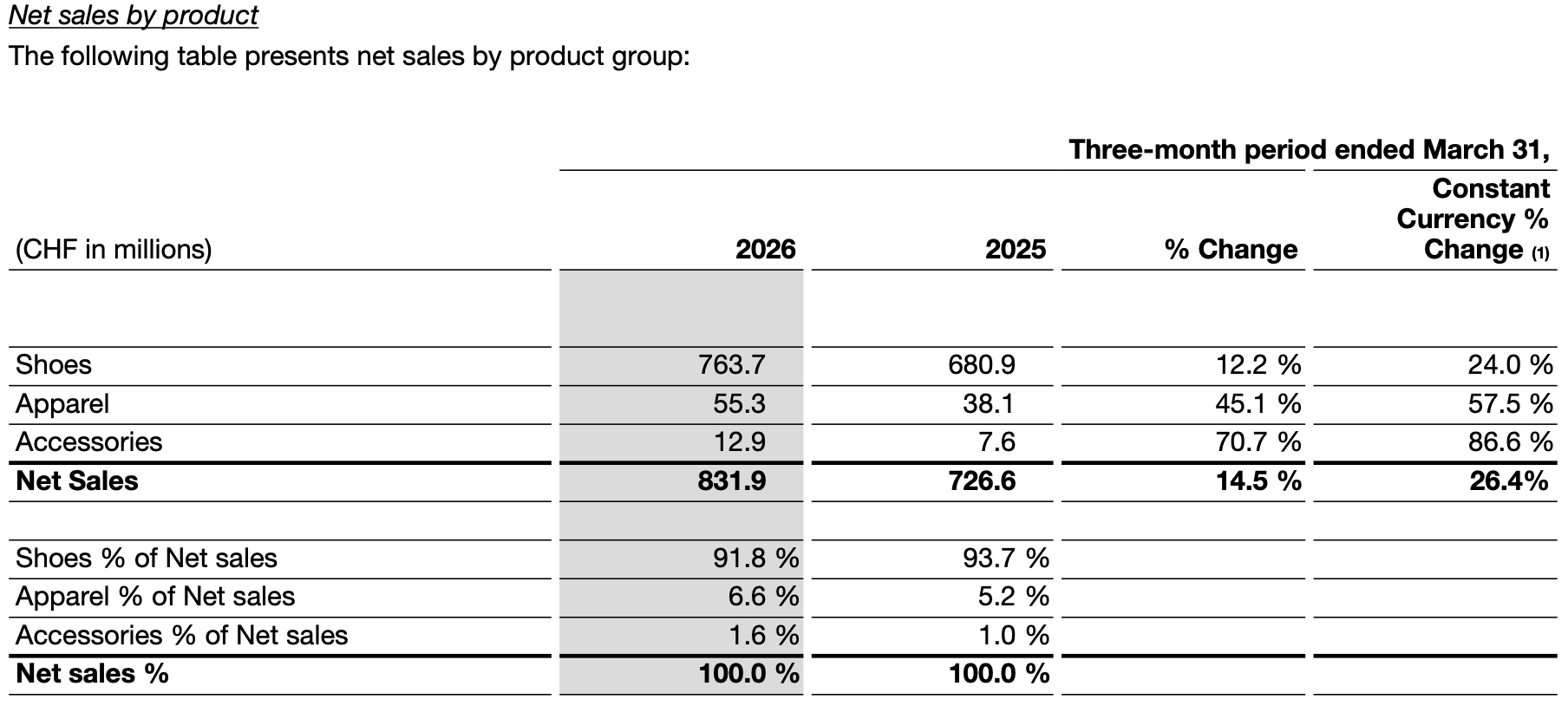

By product category:

- Footwear: net sales increased by 12.2% year-on-year to CHF 763.7 million, up 24.0% at constant exchange rates. Growth was primarily driven by best-selling core franchises, alongside meaningful contributions from new categories. The Cloudzone series, launched in early 2025 from a low base, achieved year-on-year growth of over 350%.

- Apparel: net sales increased by 45.1% year-on-year to CHF 55.3 million, up 57.5% at constant exchange rates. The category is increasingly becoming a key entry point for new customers, with rising customer lifetime value and continued optimisation in cross-category repurchase rates and purchase cycles. Apparel revenue in DTC channels exceeded 10% for the first time, underscoring its emergence as a new core growth engine for the brand.

- Accessories: net sales increased by 70.7% year-on-year to CHF 12.9 million, up 86.6% at constant exchange rates.

Looking ahead to the full year, following a strong start to 2026, On remains highly confident in its outlook. Momentum continues to build across markets, channels, and consumer communities, with its premium positioning, disciplined operations, and strong innovation pipeline supporting high-quality, margin-accretive growth. Despite ongoing macroeconomic uncertainties, the strong first-quarter performance has laid a solid foundation for the year. The company expects for full-year 2026:

- Net sales of at least CHF 3.51 billion, representing growth of at least 23% at constant exchange rates

- DTC channels, Asia-Pacific markets, and the apparel category are expected to outperform overall growth

- Supported by its full-price sales model and operational efficiency gains, gross margin is expected to reach at least 64.5% despite additional tariff pressures

- Adjusted EBITDA margin is expected to be in the range of 19.5% to 20.0%

|Source: official financial report, Reuters, analyst call transcripts

|Image Credit: brand official website

|Editor: Luxeplace